The full report is over 120-pages and you’ll find it via this link The IMF’s Annual China Report – 2026. Below I’ve filleted some of the more interesting charts for you.

In summary; the IMF would like China to get a move on in terms of stimulating domestic consumption, were surprised by the strength of the economy in 2025 and not as fussed about debt as they’ve been in the past.

Growth forecasts look modest until you work out what’s implied between now and 2030 compounded. Those not so big numbers add up to a gain of over 20% in the next five years.

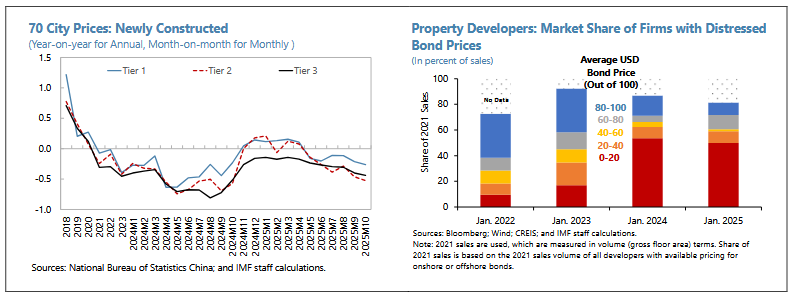

The property market isn’t out of the woods yet. The best that can be hoped for from here is stability. Full recovery is out of the question.

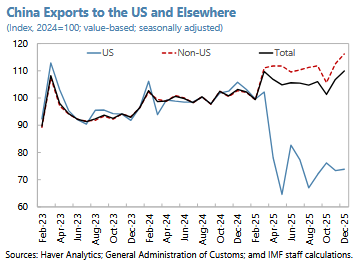

The export manufacturing complex has grown from strength to strength as a direct result of the U.S. tariff campaign. An extraordinary result.

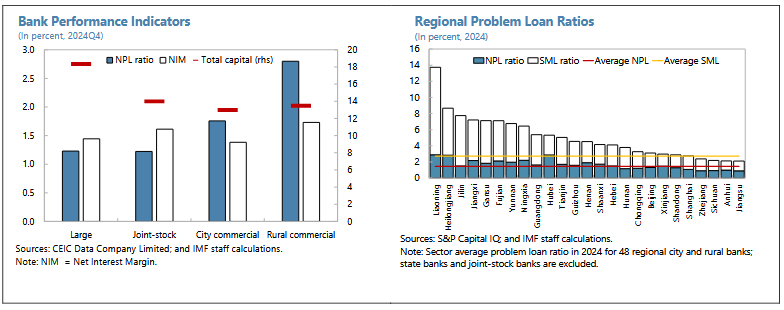

Banking sector profitability remains poor. In terms of problems though? Hard to find even if the horizon is expanded to smaller lenders.

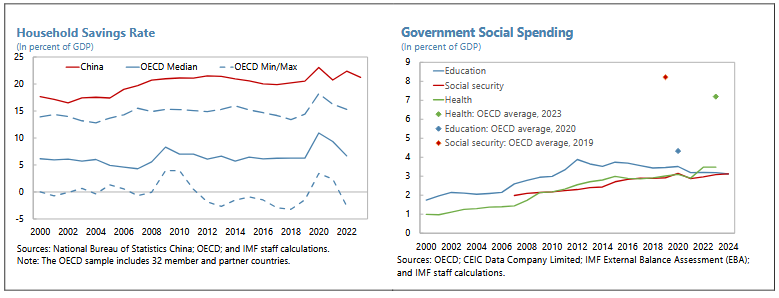

Precautionary saving remains elevated but this is in part because authorities are not (yet?) providing a strong social welfare safety net.

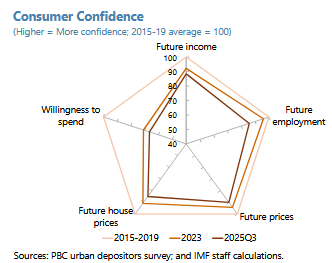

This graphic sums up the consumer neatly. They have the firepower and few worries about longer term prospects.

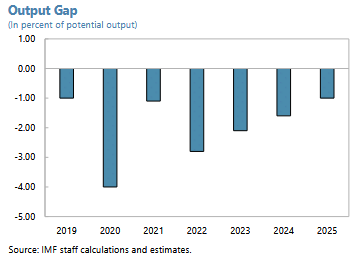

The economy continues to run below its potential. The pattern is improving but there are still productivity wins implied in this reading.

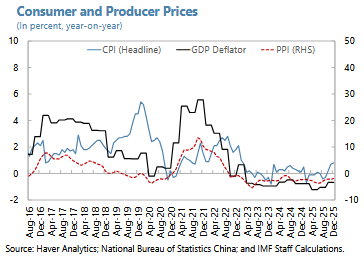

Deflation persists. I’ve never seen the problem and I’m beginning to think China’s planners don’t see one either.

At the end of the report, from P.115, there’s a response from the China side which disagrees only with the IMFs notion that China’s external position may be stronger than it reports. This dovetails also with their remarks on wanting to keep the currency stable and not using it as a trade-competition weapon.

I’d only note the currency has, in fact, noticeably weakened since 2022 which can’t have been an accident.

Happy Sunday.